If you already have a Donor Advised Fund (DAF), please designate GALDEF to receive your charitable grant on a one-time or recurring basis. Your donation helps us to support plaintiffs and their attorneys to bring impact litigation to secure children’s basic human, legal and constitutional rights to bodily integrity, to protect their future choices, and to secure redress for adults harmed as children by medically unnecessary genital surgeries (e.g. newborn circumcision and intersex genital normalization).

Genital Autonomy Legal Defense and Education Fund

1717 E. Vista Chino, A7-455 Palm Springs, CA 92262

Tel: 760.442.3133 Email: admin@galdef.org EIN: 88-3207129

If you don’t yet have a Donor Advised Fund, learn more in this article below, then consider establishing your own DAF soon and designating GALDEF for your charitable giving.

___________________________________

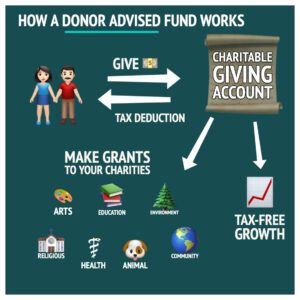

A donor-advised fund allows investors to donate directly to a charitable fund while retaining some control over the assets. Donor-advised fund administrators are public charities that qualify as section 501(c)(3) organizations.

Donors can benefit from an immediate tax deduction when they contribute cash, appreciated stock, real estate or other assets to the fund. This may also reduce or eliminate capital gains taxes. Although contributions are irrevocable (meaning you can’t withdraw donations if you change your mind or need extra cash), the donor retains an advisory role over how to invest the assets and how much to contribute to various charities over time. Any remaining assets benefit from tax-free growth as long as the account remains funded.

Main types of donor-advised funds include: those administered by a specific charity directly; those administered by a community foundation or religious organization (e.g., Jewish United Fund or Catholic Charities); and those administered by an organization connected with a financial institution (e.g., FidelityCharitable.org, SchwabCharitable.org and VanguardCharitable.org). This article deals with the last category of funds.

After the 2018 tax-law changes, which made it more difficult to deduct charitable donations for tax purposes, most investors now take the standard deduction instead of itemizing. However, rather than making smaller annual donations that might not be tax-deductible, it can be beneficial to “bunch” charitable donations into a larger donation to a donor-assisted fund in a single year, which can push you past the threshold for itemized deductions.

Donor-advised funds facilitate this strategy because donors can make a bigger contribution to a donor-advised fund in a single year and take the itemized deduction up front but still make one or more charitable contributions from the fund over time.

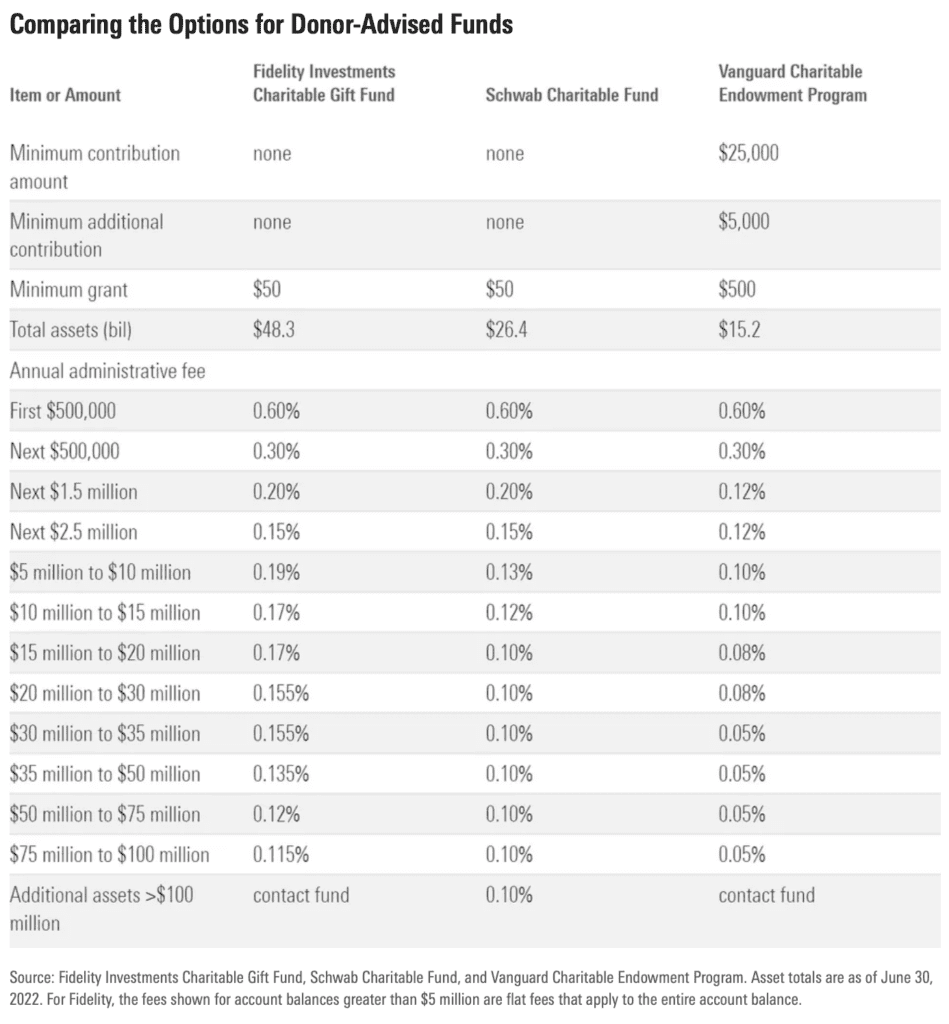

Account holders can make donations all at once or over time and to a single charity or a variety of charitable organizations. The main requirement is that donations go to a qualified charitable donor-advised fund. Each donor-advised fund sets its own minimum amount for grants to charities; Fidelity and Schwab currently have $50 minimums, while Vanguard requires a $500 minimum grant.

The table below shows how three of the largest donor-advised funds stack up. Fidelity and Schwab are accessible to the widest swath of investors because they don’t require a minimum amount for initial contributions or additional contributions, but Vanguard offers lower administrative fees for larger accounts.

All three donor-advised funds offer a range of investment options, including both diversified asset pools with exposure to a range of asset classes, and single-asset pools that can be used as building blocks for donors to put together their own portfolios. Fidelity and Schwab offer both in-house funds and third-party offerings. Vanguard’s lineup consists almost exclusively of in-house funds, with an extensive set of both index funds and actively managed offerings.

Source: https://www.morningstar.com/personal-finance/pros-cons-donor-advised-funds-3

DAFday is promoted each year on October 10 to encourage donors make their gifts via a Donor Advised Fund. Read more about DAFday here

___________________________________

Genital Autonomy Legal Defense and Education Fund

1717 E. Vista Chino, A7-455 Palm Springs, CA 92262

Tel: 760.442.3133 Email: admin@galdef.org EIN: 88-3207129

Comments are closed